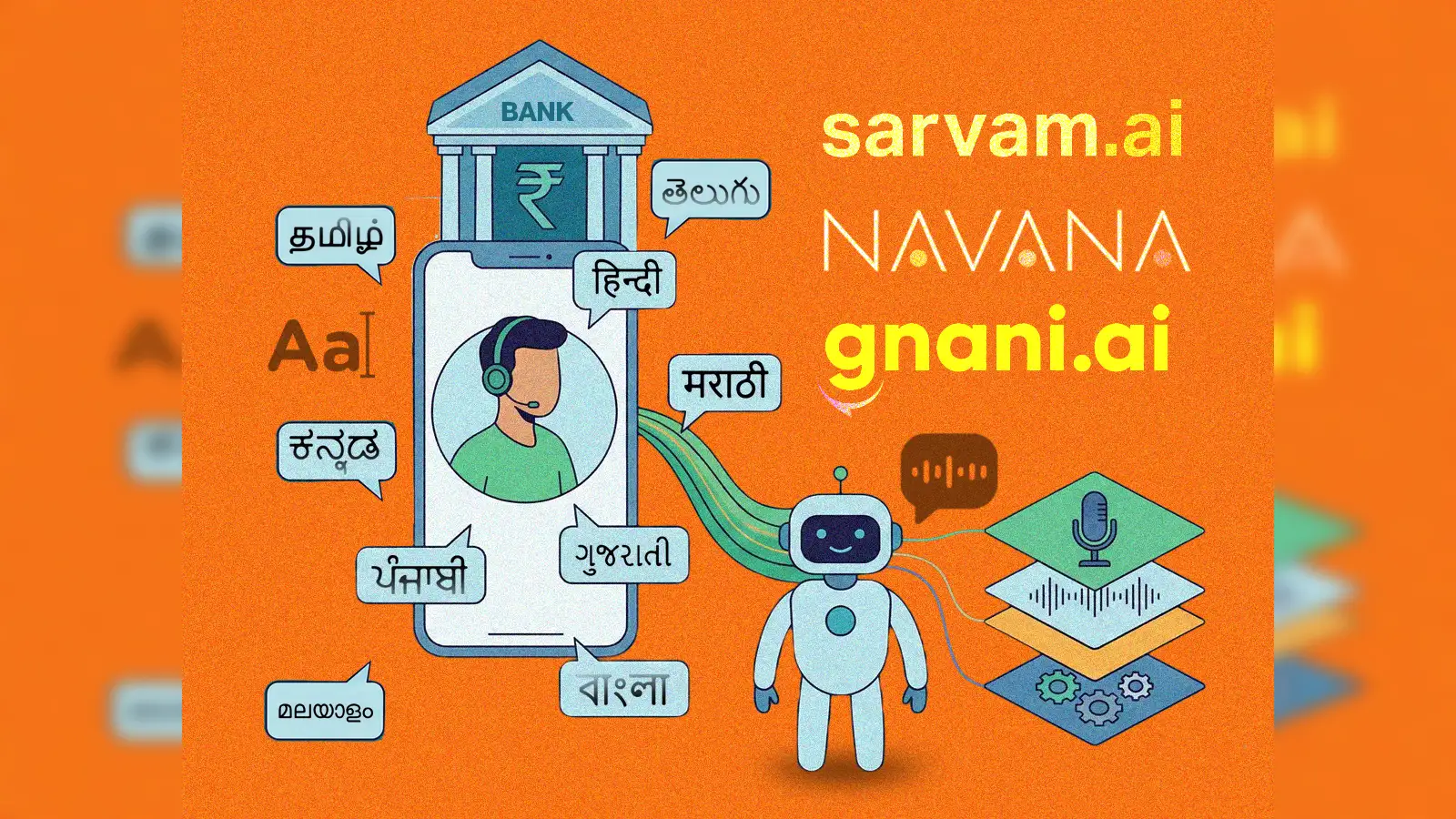

As banks tap AI for big tasks, local startups get a prompt

Large financial institutions are accelerating the use of artificial intelligence to handle tasks that were once limited to human analysts. From fraud detection to credit underwriting, banks are deploying sophisticated models that can process millions of data points in seconds. The shift is not just about speed; it reflects a broader strategy to cut costs, improve accuracy, and stay competitive in a market where digital services are becoming the norm.

Why banks are turning to AI

The pressure to modernize comes from several angles. Regulators demand tighter risk controls, while customers expect instant decisions on loans and payments. AI offers a way to meet both demands. Machine‑learning algorithms can spot patterns that traditional rule‑based systems miss, reducing false positives in fraud alerts and identifying creditworthy borrowers who might be overlooked by conventional scoring methods. In addition, automation of routine back‑office work frees staff to focus on higher‑value activities such as relationship management.

One of the most visible applications is in real‑time transaction monitoring. By analyzing transaction streams across multiple channels, AI models flag suspicious behavior within seconds, allowing banks to intervene before money moves. Another area is loan underwriting, where natural‑language processing extracts relevant information from documents, while predictive analytics assess repayment risk with greater nuance. Even wealth management is seeing AI‑driven portfolio recommendations that adjust to market shifts without human input.

Global ripple effects

The move has implications far beyond the walls of any single bank. As major players adopt AI, the technology ecosystem expands, creating demand for data scientists, cloud infrastructure, and specialized software vendors. Countries that invest in AI talent and regulatory frameworks are likely to attract more of this investment, shaping the competitive landscape of global finance. Moreover, the increased efficiency can lower transaction costs for businesses and consumers worldwide, potentially spurring economic activity.

Local startups get a prompt

While the headlines focus on the giants, smaller fintech firms are finding a niche in the AI boom. Banks often lack the agility to develop niche solutions quickly, so they turn to startups for plug‑and‑play modules. These range from AI‑powered chatbots that handle customer queries to niche risk‑assessment tools for specific industries such as agriculture or renewable energy. The partnership model allows startups to test their products at scale while giving banks access to innovative features without long development cycles.

Opportunities for collaboration

Many banks are launching accelerator programs and innovation labs to nurture local talent. These initiatives provide funding, mentorship, and access to data (in anonymized form) that would otherwise be out of reach for small companies. In return, startups deliver proof‑of‑concept solutions that can be integrated into the banks' existing platforms. This symbiotic relationship accelerates the rollout of AI capabilities across the financial sector.

Despite the optimism, there are hurdles. Data privacy regulations require careful handling of customer information, and AI models can inherit biases present in historical data. Banks must invest in model governance, explainability, and continuous monitoring to avoid regulatory penalties and reputational damage. For startups, the barrier to entry can be high; building AI solutions that meet the stringent security standards of large banks demands resources that many early‑stage firms lack.

Experts predict that AI will move from a supporting role to a strategic one within banking. As models become more transparent and regulatory frameworks evolve, banks may rely on AI for strategic decision‑making, such as determining market entry or pricing new financial products. Meanwhile, the ecosystem of local innovators is expected to grow, driven by the need for specialized tools that address regional market nuances.

What it means for consumers

For the everyday user, the convergence of AI and banking promises faster service, more personalized offers, and stronger protection against fraud. However, it also means that personal data will be processed by increasingly complex algorithms, underscoring the importance of robust privacy safeguards. Consumers can expect a gradual shift toward digital‑first experiences, with human interaction reserved for more complex or sensitive matters.

In summary, the adoption of artificial intelligence by major banks is reshaping the financial industry on a global scale. The technology unlocks efficiencies, enhances risk management, and creates a fertile ground for local startups to innovate. As collaborations deepen and regulatory frameworks catch up, the combined momentum of large institutions and agile newcomers is set to drive the next wave of financial transformation.